Startup Bookkeeping 101: Cost of Goods Sold (CoGS)

- Chris Woodham

- May 1

- 3 min read

The next section of your Profit and Loss is Cost of Goods Sold (CoGS). This section includes all of the direct expenses associated with producing the product or service you sell. SaaS P&Ls will include items such as Engineering, Hosting, Product, etc. These accounts will include both payroll and non-payroll expenses. Separating these direct costs from administrative and other non-operating costs allows us to begin basic analysis of the profitability of your business.

Gross Margin

Gross Margin Ratio is one of the first ratios we look at when evaluating the health of a business. It is calculated as follows: (Revenue - CoGS)/Revenue. This basic ratio shows how much of your revenue is spent simply producing the revenue itself and how much is left over for overhead expenses. If your Gross Margin is negative you immediately know you are spending more to produce your product than you receive by selling it. Sometimes this is a scaling issue and as you grow your business your revenue growth will outpace your expenses. In other cases there may be fundamental problems with your business model. By calculating this ratio you can compare your results to industry benchmarks and begin evaluating your results beyond the basic numbers.

What Expenses Should You Include?

The easiest way to determine if an expense is included in CoGS is to ask if the product or service can be delivered without it. A lawn care company would include payroll for workers, gas for the mowers, and transportation to and from job sites. SaaS includes hosting, engineering, customer success, and any other expenses that directly or indirectly support the product itself. This does not include departments such as HR, marketing, or accounting that may occasionally support the product by assisting with pricing decisions, market research, etc. but whose primary purpose is to support the business behind the product.

Because of how important Gross Margin and the Gross Margin Ratio is it is vital that expenses are correctly included or excluded from CoGS. Including non-CoGS expenses in CoGS will reduce your Gross Margin Ratio and give a bleaker picture of your business and vice versa. If you have any questions regarding this split please feel free to reach out for a consultation or work with your existing bookkeeper to ensure everything is categorized properly.

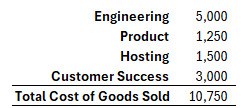

Summary and Detailed CoGS Views

The first example we will look at is very high level. Here we have rolled up the expenses by department into single line items. Using QuickBooks Online your bookkeeper will still record each expense to it's correct account such as travel, payroll, training, etc. By using Departments we can then produce summarized reporting as shown above while maintaining the accuracy of the underlying books. This view is typically used for high level summaries as it allows stakeholders to quickly identify areas where more attention is needed without getting too bogged down in the weeds. Please note some key accounts such as hosting may fall under a particular department's budget but are typically split out on this summary review. Doing some initial work with your bookkeeper to determine which accounts should be summarized vs. reported separately will set you up for success going forward.

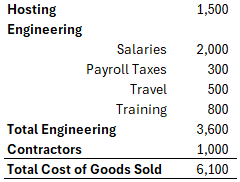

The next example we will look at breaks out the expenses by department and type. This is the more granular view and allows you to review your expenses in more detail. The same basic structure of the Summary view is still followed but each summarized account will be expanded to show exactly where the money was spent within each category. This view will allow you to hone in on any problem areas and fill in the details of the story told by the Summary view.

Reviewing Cost of Goods Sold

The typical review flow starts with the Summary view. If any of the high level categories are unexpectedly high or low compared to budge or prior months we move on to the Detailed view. We can then identify which line items are causing the variance. Sometimes this is enough to jog the reviewer's memory and the variances can be explained immediately. In others cases the account detail reports may be needed to identify the cause of the variances. In either case you bookkeeper should be able to provide the relevant information at the right level of detail to explain any variances you wish to examine.

Final Thoughts

CoGS is an important part of your P&L and should be reviewed on a monthly basis. This is the main contributor to the efficiency of your business. The lower your CoGS the higher your Gross Margin leading to more money being available for administrative and other overhead expenses, ultimately leading to more money left for owners. By accurately categorizing CoGS expenses and diligently reviewing them each month you can catch problems before they have a chance to grow.

Comments